The much-awaited March rate decision from the Federal Open Market Committee (FOMC) is now at hand, and the U.S. dollar, which has been rangebound since the start of the year, continues to struggle to decisively breakout above the key 100 psychological resistance level.

Can Wednesday’s Fed decision provide a thrust to the dollar, giving it a decisive upward momentum?

What Should Traders Expect from the Fed? A pause decision is almost a certainty when the Federal Reserve releases the post-meeting policy statement Wednesday afternoon. The odds of a pause is at 98.9%, according to the CME FedWatch Tool, which factors in the expectations of futures traders. A hot producer price inflation (PPI) report released Wednesday morning has doused any lingering hopes for a rate cut. In fact, the futures market began pricing in 1.1% odds of a quarter-point hike to 3.75%-4.00%.

Here’s a compilation of some economists’ expectation:

- Morgan Stanley economist sees the central bank adopting a wait-and-watch approach as it debates the outlook, including the degree to which employment has stabilized, the risk higher oil prices pose for inflation and activity, and the appropriate path for monetary policy.

- ING Senior Rate Strategist Benjamin Schroeder said Fed Governor Stephen Miran could dissent yet again in March.

Fed Chair Jerome Powell’s press briefing in which he would explain the thinking behind the rate decision and the monetary policy outlook would also be closely watched by traders.

Read on Rate Outlook: Morgan Stanley prefers focusing on the dot-plot chart, a graph which shows each policymaker’s expectation where rates would be in the future, and the Summary of Economic Projections (SEP). The firm expects the dot-plot chart to show one rate cut this year, and another next year.

ING, meanwhile, expects the central bank to trim its growth forecast slightly and nudge up its inflation forecast, while also delaying the rate cut to 2027.

Will Oil Shock Sway Fed? Since the Fed’s January rate-setting meeting, the Middle East tensions involving the U.S. and Iran have pushed Brent crude past $100 as the Strait of Hormuz remains blocked for shipments. While WisdomTree Senior Economist Jeremy Siegel said oil’s spike should not push the FOMC members to become more hawkish, reasoning that it is a supply shock, and not one driven by excess demand or excessive credit creation.

But even before the Middle East crisis, inflation continued to remain stubbornly above the central bank target. The February inflation reading released earlier this month showed annual consumer price inflation (CPI) rate at 2.4% and the core rate at 2.5%, above the central bank’s 2% target. Consumer inflation expectations also stayed elevated, with the mid-month readings of University of Michigan’s March survey showing one-year and five-year inflation expectations at 3.4% and 3.2%, respectively.

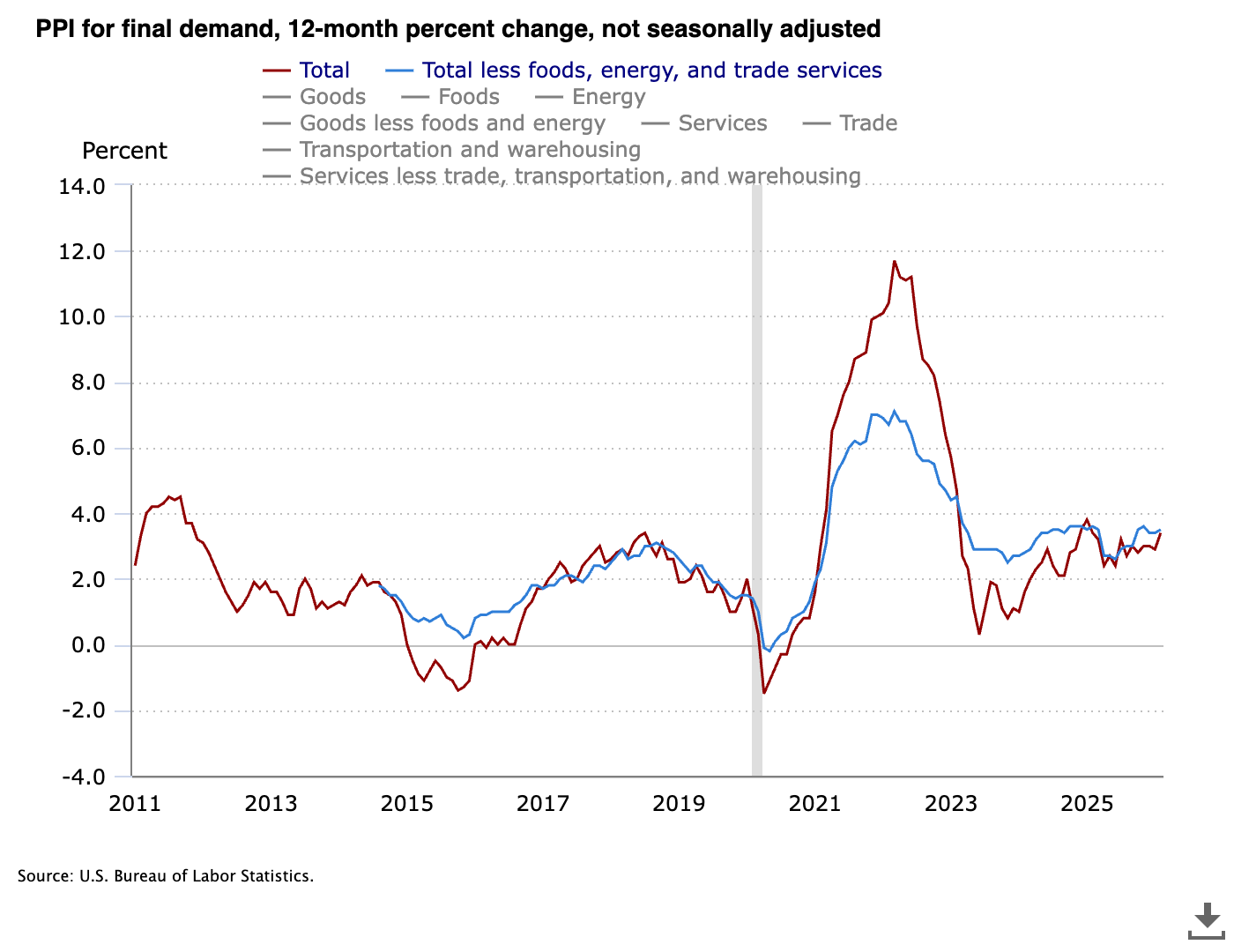

More evidence of inflationary pressure emerged on Wednesday as the Bureau of Labor Statistics’ (BLS) PPI report for February showed pricing pressures at the wholesale level that exceeded expectations. The annual headline inflation rate of 3.4% marked the highest since January 2025.

Annual Producer Price Inflation

Source: BLS

Goods prices jumped 1.1% month over month (MoM), pushed higher by food and energy prices, which climbed 2.4% and 2.3%, respectively.

Charles Schwab Center for Financial Research Head of Macro Research Kevin Gordon said the PPI print points to another firm price consumption expenditure (PCE) data for February.

Dollar Stuck Below Key Level: The U.S. dollar futures dropped to a nearly four-year low in late January but has staged a comeback since. The contract tied to the U.S. dollar Index that measures the value of the greenback against six major global currencies, breached the 100 barrier in a couple of sessions but only to retreat below the mark soon after.

For the year-to-date period, the DX contract has gained 1.3%.

Dollar Index Futures (1-Year Chart)

Source: TradingView

Commenting on DX’s trajectory, LPL Chief Technical Strategist Adam Turnquist weighed in on the factors that lent support to it this year. These include:

- Dimming hopes of Fed funds rate cut this year

- Safe-haven demand amid the multiple headwinds

- Diverging monetary policy paths among major global central banks

- Short-covering following the Iran war

Weighing in on the technical setup for the dollar index, Turnquist said “a decisive break above 100.5 would confirm a breakout and set a minimum technical target near 105.” On the other hand, a pullback would take the index to a support around 99.48. If the support fails to hold, the index could retreat toward its 100-day moving average around 98.62.