Stagflation, a term referring to the unusual combination of elevated inflationary pressure and low growth, is making headlines yet again. Search volumes for the term began to rise in March, climbing to the highest since May 2025, as incoming data reinforced the stickiness of inflation and softening of growth.

Friday brought a raft of economic data that fit the textbook definition of stagflation. More concerning, however, is that numbers reflect conditions before the onset of the U.S.-Iran war, a conflict that now threatens to further derail global economic momentum.

A Wall Street Voice Warns: Bank of America strategist Michael Hartnett drew a parallel between 2008 and the present time. In a note to clients, the BofA strategist pointed to risks such as a spike in oil prices, banks’ exposure to the private credit market that has begun to show cracks, Bloomberg reported.

Unlike most market participants who worry about inflation, Hartnett expressed concerns about the impact of the oil shock and tightening financial conditions on corporate earnings.

Against the backdrop, Hartnett has these recommendations for investors:

- Fade the oil rally above $100-a-barrel.

- Sell 30-year Treasury bonds when yield tops 5%.

- Sell the dollar when the spot dollar index (DXY) trades above 100.

- Sell S&P 500 Index when it drops below 6,600.

The Brent Crude futures contract trading on the Intercontinental Exchange (ICE) has topped $100, and DXY trades over 100, while the 30-year Treasury yield is at 4.9% and the S&P 500 Index is holding above 6,600.

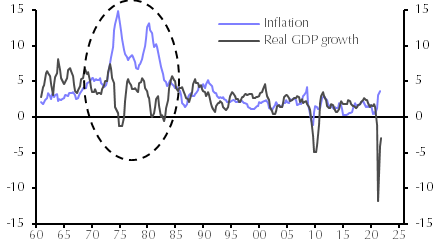

Deja Vu? There is an eerie similarity between how the macro environment is shaping up currently and the 1970s stagflation in the U.S. The latter was caused by the spike in oil prices following Oil and Petroleum Exporting Countries’ (OPEC) embargo in 1973, with the situation exacerbated by increased government spending and the collapse of the Bretton Woods system.

Inflation Vs Real GDP Growth

Source: Capital Economics

The nearly decade-old stagflationary environment was reined in by former Federal Reserve Chair Paul Volcker’s steep interest rate hikes. While Volcker’s rate hikes cured inflation, a Fed funds rate as high as 20% pushed the economy into on and off recessions within the stagflationary period.

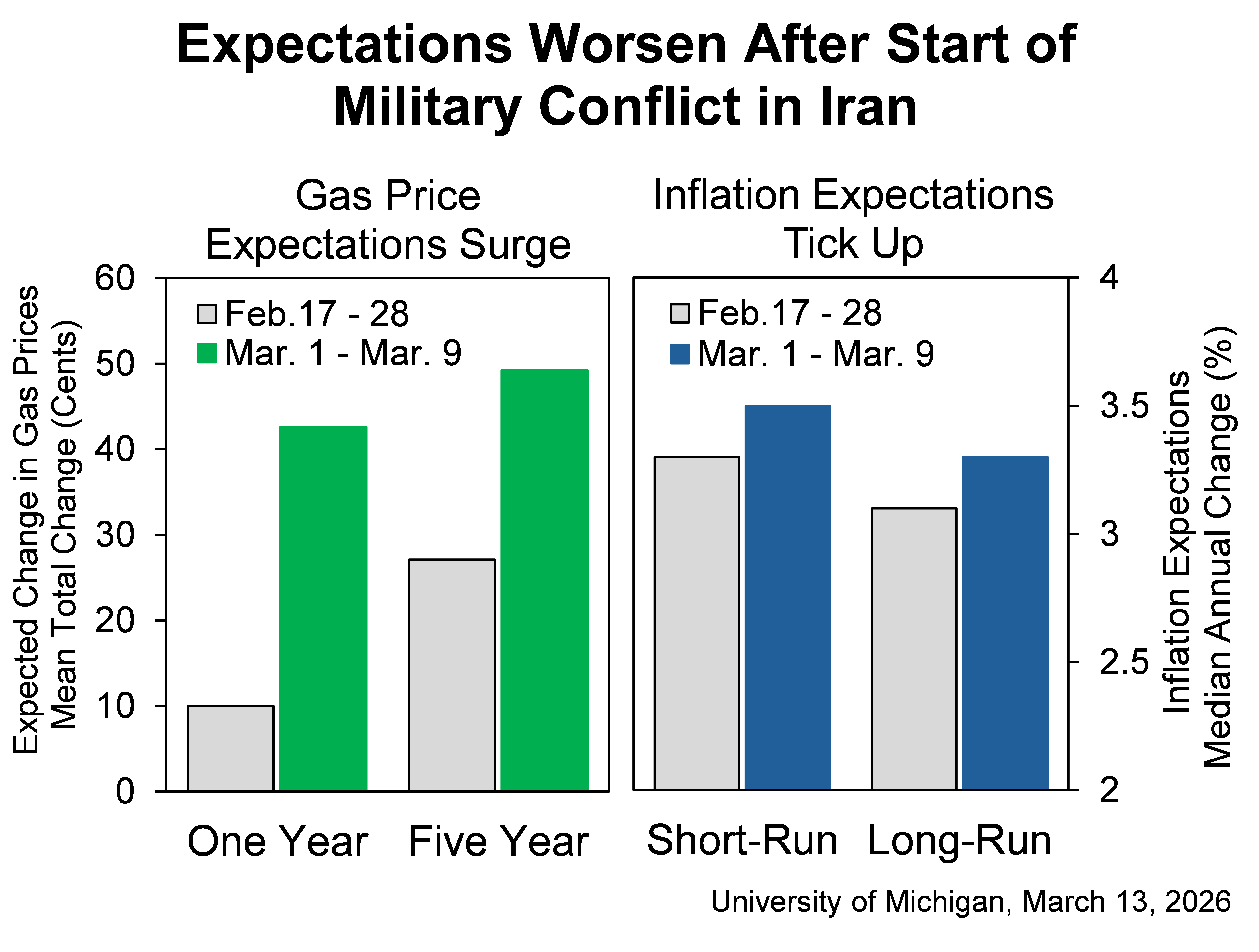

What UMich Survey Says: The mid-month reading of the University of Michigan’s March survey showed the headline consumer sentiment index fell 1.9% month-over-month to 55.5. The index was down 2.6% from the year-ago period.

The survey was conducted between Feb. 17 and March 9.

Director of the survey Joanne Hsu said readings collected before the Iran war showed a cheery mood among consumers, although those received during the nine days after that erased the early gains. Higher gasoline prices remained a key concern for consumers.

The consumer expectations index fell 4.4% month over month to 54.1 but climbed nearly 3% from a year ago.

The survey showed that one-year inflation expectations snapped a six month declining streak, stalling at 3.4%. The longer-term inflation expectations edged down to 3.2%. Both, however, came in tamer than the 3.6% and 3.4% rate estimated by economists.

Source: University of Michigan

Job Market Far from Causing Concern: Job openings as well as labor turnover changed little in January, the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS) showed. The number of job openings was at 6.946 million versus the upwardly revised 6.550 million for December. Economists, on average, estimated 6.760 million job openings for the month. Firings remained steady at 5.1 million.

Fifth Third Bank Chief Economist Jeff Korzenik said the unexpected increase in job openings reflected the end of tariff policy paralysis and employers’ continuing to absorb the impact of the immigration policy change.

Where does this take the monetary policy? These data corroborates the PCE inflation reading received Friday as part of the personal income and spending report for January. That said, the sharp downward revision to fourth-quarter U.S. GDP growth complicates the outlook for monetary policy.

LPL Chief Economist Jeffrey Roach said, “Underlying inflation pressures will continue to boil under the surface and next month’s print will also be elevated, impacted by the war in the Middle East.”

In the March meeting policy statement, the Fed will likely highlight the uncertainty on both sides of the mandate. The economist also braces for some important revisions in the upcoming Summary of Economic Projections (SEP) next week.