Things look grim for the global energy market, specifically for Liquified natural gas (LNG), a refined product from natural gas. The retaliatory attacks carried out by Iran late Wednesday and Thursday morning have left Qatar’s Ras Laffan Industrial City, the world’s largest LNG hub and export facility, crippled.

So, is that a big deal? It appears so, going by a statement put out by QatarEnergy, the world’s largest producer of LNG. The firm warned of a prolonged disruption that would take up to five years to repair and a $20 billion hit to its topline. The dire prediction comes as the firm suffered extensive to some of its infrastructure, which includes:

- Two LNG producing trains, named Train 4 and Train 6 which the company operates along with U.S. giant Exxon Mobil

- Pearl Gas-to-Liquids (GTL) facility which QatarEnergy operates along with British oil company Shell; This unit converts natural gas into cleaner-burning drop-in fuels and also produces base oil used to make premium engine oils, lubricants, paraffins and waxes.

It has to be noted here that immediately after the start of the war (March 2), production at Ras Laffan was temporarily halted following earlier drone attacks.

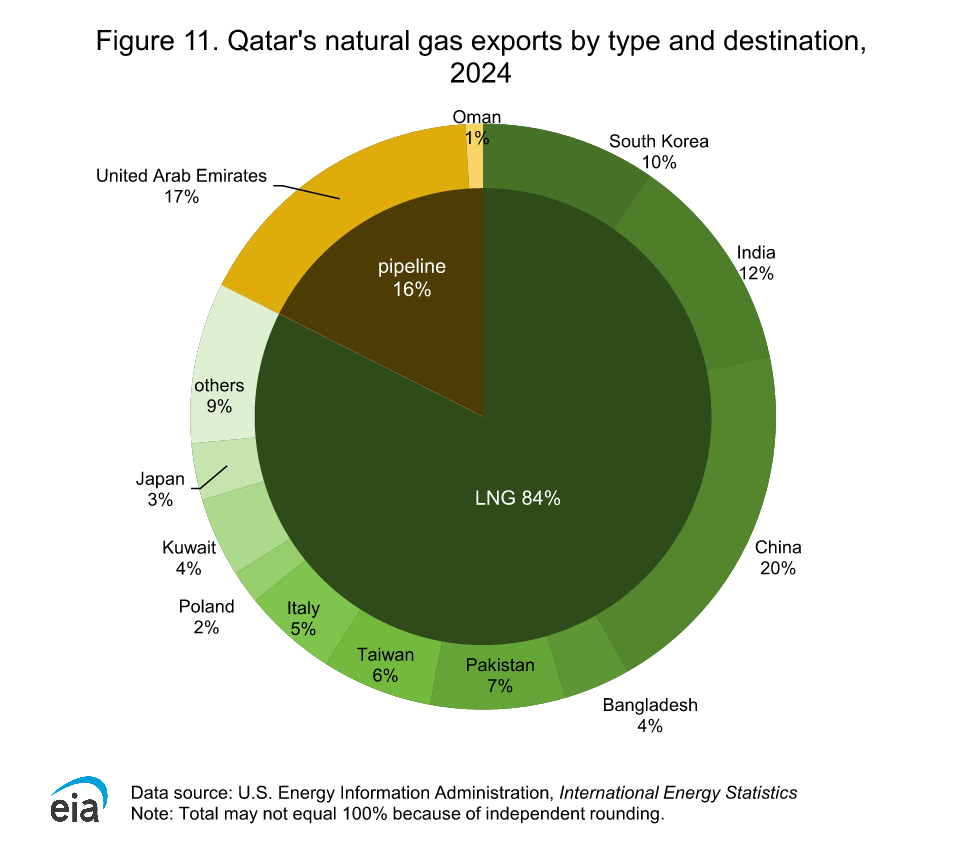

What’s At Stake? Train 4 and Train 6 collectively produce 12.8 million tons per annum (MTPA) of LNG, accounting for 17% of Qatari exports. QatarEnergy said it may have to declare force majeure, a clause in contracts which frees the supplier and procurer from liability or obligation in the event of an extraordinary event, for up to five years on some of the long-term contracts with China, South Korea, Italy and Belgium.

One of the two trains of the Pearl GTL facility is expected to remain offline for at least a year. The outage is also expected to hit the production of associated products such as condensates, naphtha, sulfur and helium.

Source: EIA

So, does this partial hit impact the global LNG market in a big way. The global LNG trade was at more than 550 billion cubic meters (bcm) in 2025, according to a quarterly gas market update from the International Energy Agency (IEA). The 12.8 MTPA of LNG (equivalent to 18 bcm) disruption in Qatar would remove roughly 3%-4% of LNG off the market.

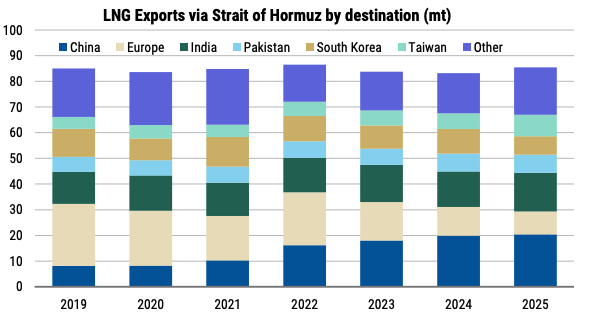

As the Strait of Hormuz, the chokepoint in the Persian Gulf remains blocked due to the ongoing war, about 5%-10% LNG supply reduction is anticipated, assuming that for every month of the strait’s closure about 7.6 bcm of LNG exports would be lost .

About 70% of LNG export through Hormuz go to Asia, and 10% to Europe.

Source: Morgan Stanley

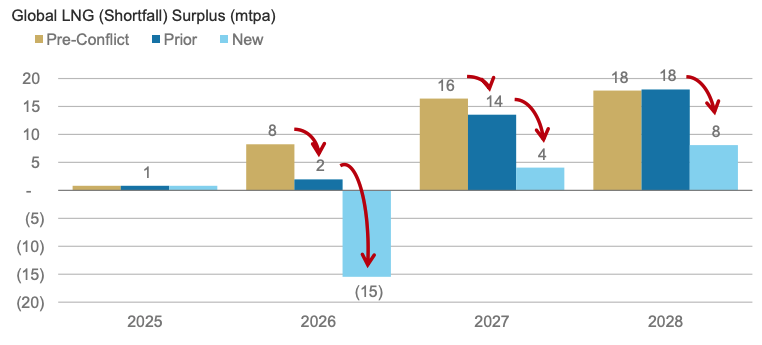

In a report released Friday, Morgan Stanley Commodity Strategist Devin McDermott said, in the wake of the recent escalation, the firm assumes a complete two-month outage at Qatar and also the impact of two trains remaining fully offline through 2028. The anticipated shortfall is expected to be partly offset by slower demand growth.

Source: Morgan Stanley

EU Choked: The development could not have come at a worse time for Europe. The European Union (EU), which imported 142 bcm of LNG in 2025, would feel the pinch the most.

A small 3%–4% global LNG shock translates into a disproportionately large crisis in Europe due to the region’s structural reliance on LNG, slumping Russian imports and very little scope for expanding pipeline supply from elsewhere, which has already been maxed out.

Apart from tanker shipments, the 27-nation bloc imports pipeline supplies to the tune of 150-200 bcm per year, mainly procured from Norway, North Africa, Azerbaijan and Russia

Russian exports have already dwindled, having fallen to 13% in 2025 from 40% before the 2022 Ukraine war began. As recently as in January, the European Union countries approved a total ban of Russian gas imports by the end of 2026 and pipeline gas supply by Sept. 30, 2027. A ban on spot imports came into effect on March 18, with futures contracts to be phased out over the next two years.

Top Gas Suppliers to EU (2025)

Source: European Commission

Prices Skyrocket: The supply concerns manifested in the form of a spike in the futures market. The Dutch Title Transfer Facility (TTF) Natural Gas futures, the European benchmark, and the UK NBP Natural Gas futures and the LNG Japan/Korea Marker (Platts) futures all reacted to the supply crisis. On Thursday:

- The TTF futures jumped over 13% on Thursday to 61.90 euros per Megawatt-hour (MWh), trimming some of their intraday peak gains of nearly 27%

- UK NBP futures soared nearly 11.5% to 152.62 pence per therm

- The Asian benchmark, the LNG Japan/Korea Marker futures, gained nearly 11% to $22.35 per million British thermal units (MMBtu).

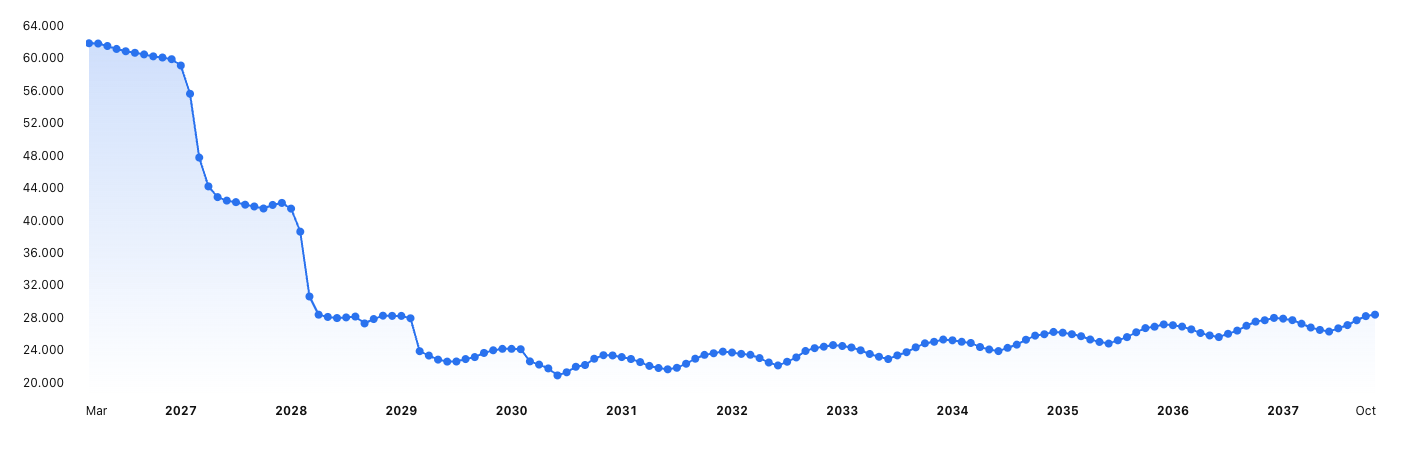

The TTF futures forward curve suggests prices will remain at pre-US-Iran war levels at least until March 2028 and then moderate thereafter. The futures forward curve, obtained by plotting prices of contracts across future delivery dates, gives market expectations regarding prices in the future.

TTF Natural Gas Futures Forward Curve

Source: TradingView

Cascade Effects Feared: The impact of the rising gas prices is expected to reverberate across sectors, industries and companies, and economies as well as the governments.

- If the disruption persists beyond the Spring shoulder season, when renewable energy production typically complements supply, industries may have to switch to alternative fuels such as coal and lignite, according to Julius Baer Head of Economics Norbert Rucker.

- Energy-intensive industries such as chemicals, steel and glass, which use gas as feedstock, will likely see cost escalation or paucity. JPMorgan estimates that European chemical companies may have to raise their selling prices by more than 5% over the next 12 months to combat higher energy prices. If they are not able to pass through all input price increases, they might have to take a hit to their bottom line.

- Higher gas bills could eat away at consumers’ disposable income, leaving them very little to spend elsewhere. This in turn could lead to demand destruction, hurting economic growth. The NYMEX-traded RBOB Gasoline futures prices have climbed about 49% since the war started.

- Among industries, high-tech industries such as chipmakers and consumer electronics manufacturers may also face the heat. Helium, a byproduct of natural gas processing, is used in advanced chip manufacturing used in artificial intelligence (AI) applications and also as cooling gas and shielding gas during fabrication of semiconductor wafers. Chips now account for over one-fifth of global helium demand. The Ras Laffan facility, which has suffered extensive damage, extracts and liquefies up to 17 metric tons of helium per day. This in turn will squeeze chip supply chains, potentially raising prices for end products.

As companies face the double whammy of higher input prices and demand slowdown, corporate profit growth, which has been one of the main engines of economic growth in the current cycle, would likely slow down. This poses a downside risk to equity markets, especially the tech-heavy indices. Quite rightly, JPMorgan cut its 2026 year-end forecast for the S&P 500 Index, a broader U.S. equity market gauge, to 7,200 from the 7,500 it estimated earlier. The firm stated that investors haven’t fully factored in the impact of the energy shock or the second and third-order effects it could create.

Most central banks, which held their policy-setting meetings this week, expressed uneasiness over the inflation-stoking effect of the higher energy prices in the aftermath of the Middle East tensions. While most said the higher energy prices introduce uncertainty with respect to the growth and inflation outlook, for now they were willing to shrug off any impact as transitory. This is based on the most optimistic assumption of the crisis ending within the next one to two weeks.

If the oil prices stay high for a prolonged period, the central banks would be left with no option but to raise rates, rather than the cuts, as most had been discussing until recently.