Gold has officially entered a bear market, stalling a bull run that lasted for more than three years. The sell-off in the yellow metal has intensified since the start of the U.S.-Iran war, which has now entered its 24th day.

In the past week alone, gold futures fell nearly 17%, marking the steepest weekly drop in more than 40 years.

What Has Broken the Back of Gold’s Rally? The reversal of key tailwinds, particularly a weaker dollar and rate-cut expectations, has left gold exposed to broad liquidation pressures. The dollar has gained more than 1% this year and the war clouds have dimmed the outlook for rapid rate cuts which the market was hoping for. The safe-haven appeal of gold has not held up his time as the deterioration in the geopolitical milieu did little to support prices.

Bear Market Reckoner: Technically, a bear market is defined as a pullback of more than 20% from a previous high. Assessing the current downturn requires a comparison with historical cycles to evaluate whether the present phase is cyclical or indicative of a more secular shift.

Since the 1970s, gold has gone through multiple bear phases, and the most recent ones were

- The 2022 bear market lasted for about 225 days, or roughly 160 trading sessions.

- The 2013 bear market, which came amid the extended gold bear phase of 2011-2015.

Rate-Shock Bear Market: Gold futures peaked (intraday) at $2,072 on March 8, 2022, before hitting a cycle low of $1,637.50 on Oct. 19, 2022, a peak-trough drawdown of 21% over

The downturn in the commodity came as global central banks began aggressively hiking interest rates after cutting them to near zero in the aftermath of the COVID-19 pandemic. The extremely accommodative monetary policy stance had fueled inflationary pressures, leaving central banks with little option but to tighten policy.

A rising interest rate environment supported the dollar, which climbed more than 19% in 2022 to a late-September peak, marking its highest level in nearly two decades. Rising real yields also acted as a headwind for gold.

Source: TradingView

Nevertheless, the 2022 drop is widely viewed as a rate-driven plunge within a broader secular bull market, and the yellow metal rebounded once the macro narrative lifted. Unlike the previous multi-year bear cycles, this one was a single-cause, single-year event. Once the hiking cycle peaked, the dollar strength waned, helping an explosive rebound by the gold. During this period, gold received some support from the Russia-Ukraine war, mitigating some of the weakness. In a stricter sense, 2022 should be called a correction, rather than a bear market.

The contract tied to gold ended the year little changed and then launched into a multi-year rally. With the Fed signaling that rate hikes were drawing to a close, which in turn weakened the dollar and the real yields, gold began a multi-year rally. Central bank purchase of gold gained ground, lending support.

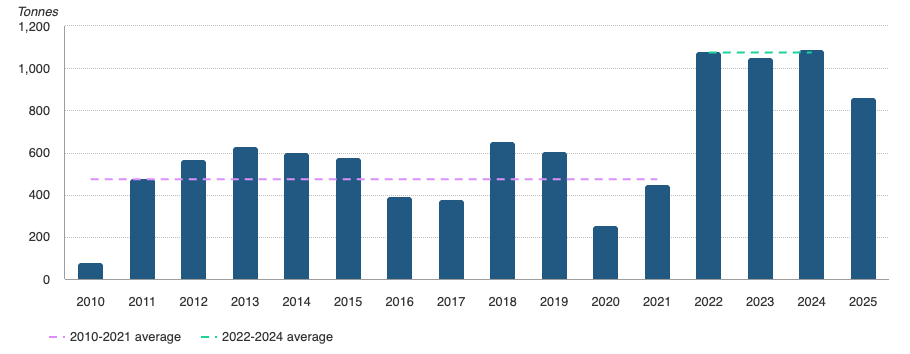

Central Bank Net Gold Purchases

Source: World Gold Council

The annual gains after the 2022 setback:

- 2023: +13%

- 2024: +28%

- 2025: +65%

2011-15: Bear Market Kicks Off as Safe-Haven Demand Erodes: The Great Financial Crisis (GFC) of 2007-09 and the Eurozone debt crisis that began in 2008 had fueled a rally in gold that strengthened a multi-year rally that peaked in September 2011. As the global economy emerged from the GFC and risky bets returned to be in favor, investment dollars shifted out of safe-haven gold into equities and bonds. The S&P 500 Index, a measure of broader market performance, gained 30% in 2013 and 11% in 2014.

Also, the Federal Reserve announced its intention to taper quantitative easing, which pushed up bond yields and strengthened the greenback. The QE ended by October 2014 and the Fed began hiking interest rates, beginning in December 2015.

Gold was also pressured by a rise in real interest rates, which are the nominal interest rate adjusted for inflation. As real interest rates increased from negative territory, holding gold, which is a non-yielding asset, became less attractive.

The end result was a four-year long bear phase, with the year 2013 seeing a flash crash.

Source: TradingView

After bottoming at $1,046.20 in early December, gold reversed course and began a multi-stage recovery as the macro headwinds reversed. As the dollar weakened amid Fed’s policy pivot, central bank purchases increased, especially from Russia and China, and emerging market demand firming up, gold found its feet and generated positive returns for 2016 (+9%) and 2017 (+14%). After clocking a modest 2% loss in 2018, the yellow metal rallied amid the pandemic before going into a consolidation move.

How Would Gold Headwinds Play Out This Time? History says not geopolitics but a confluence of real yields, U.S. dollar and interest rate outlook drive sustained trends in gold.

ING Commodities Strategist Ewa Manthey says: “More broadly, geopolitics alone rarely drives gold prices in a sustained way; what matters is how such shocks feed through to inflation, monetary policy and the dollar. In the near term, a stronger US dollar and gold’s high liquidity can make it a source of funds during stress episodes.”

Therefore, the Middle East crisis per se may not support gold but the offshoots of the war could.

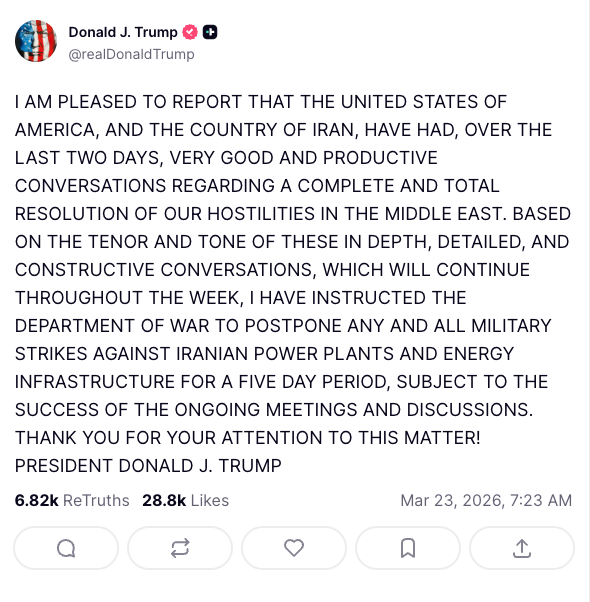

Where is the Iran-US war headed? Although no concrete resolution is in sight, U.S. President Donald Trump has taken a step back. In a Truth Social post early Monday, the president said he has ordered pausing strikes against Iranian power plants for a five-day period after giving a 48-hour ultimatum on Saturday.

The development has pushed crude futures sharply lower but gold futures continue to trade lower, although off their lows.

Will Macro Burn Gold? The risk of rising inflation persists until a lasting solution is achieved. After leaving rates unchanged at the March rate-setting meeting, Fed Chair Jerome Powell has signaled that further progress in inflation is essential for rates to drop from current levels. A higher-for-longer rate environment could pose a headwind for gold.

ING strategist Manthey, however, remains constructive on gold but acknowledges that near-term risks have increased. Despite all the noise and the pullback, gold is still up marginally for the year. According to Manthey, this leaves gold vulnerable to bouts of profit-taking. “However, any deeper pullback would likely attract buyers, particularly from central banks and longer-term investors,” she added.