The U.S. Dollar Index futures (DX) climbed above a psychological level on Friday as geopolitical tensions in the Middle East continued unabated and the fate of next week’s Federal Reserve rate-setting meeting has almost been sealed.

In the early European session, the contract tied to the U.S. Dollar Index, rose to as high as 100.29. The derivative instrument has since pulled back although it still held above the 100 mark.

Dollar Index Futures (1-Year Chart)

Source: TradingView

Bracing for Prolonged Oil Disruption: The U.S. Dollar’s appeal as a safe-haven asset has come to the fore as investors increasingly price in the risk of a prolonged disruption. The blockade of the Strait of Hormuz, a narrow waterway linking the Persian Gulf with the Gulf of Oman and the Arabian Sea and a major chokepoint, has stalled oil and natural gas shipments from Gulf producers, heightening concerns over global energy supply.

ING strategists said investors attached a merely 40% odds of traffic through the strait returning to normal by the end of April, down notably from 79% early this week. “The market probably has little confidence that Iran can be bombed into submission and instead will be looking for any paths to a halt in hostilities, be that through a ceasefire or Washington declaring ‘mission accomplished.’”

US Insulated? The dollar’s resilience is also a function of the U.S.’s energy independence, said Danish investment bank Saxo. The firm noted that the country relies very little on oil and gas supplies that are routed through Hormuz.

The U.S. became a net exporter of total petroleum products in 2020. However, the country still imports heavier crude grades to feed its refineries, and exports finished products such as distillate fuel, motor gasoline and jet fuel.

Fed To Stand Pat? The Federal Open Market Committee (FOMC), the Fed’s rate-setting committee, which meets next week, is widely expected to hold fire. This is despite the political pressure to lower rates. In a late Thursday Truth Social post, U.S. President Donald Trump implied that the central bank should convene an emergency meeting to announce a rate cut.

Recent labor market readings have been encouraging and pre-Iran war inflation reading showed prices remaining stubbornly above the central bank target.

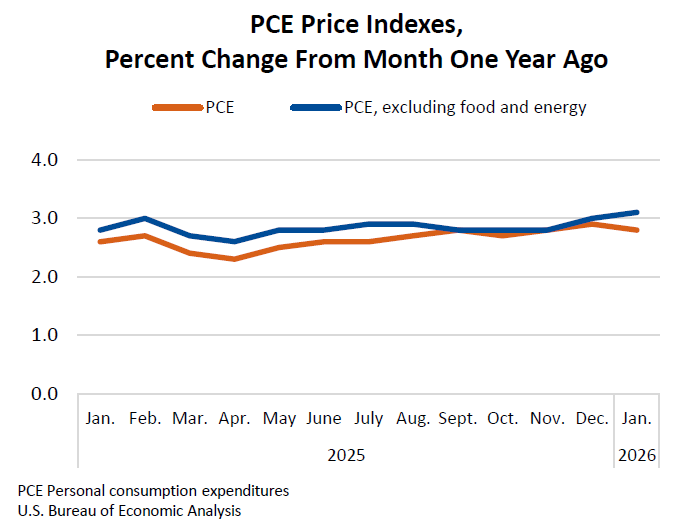

Mixed Data Confounds Outlook: The price consumption expenditure (PCE) index, released as part of the January personal income and spending report rose 2.8% year over year (YoY) in January, according to a Bureau of Economic Analysis report published Friday. The consensus estimate called for a 2.9% rate, flat with the level seen in December.

The Fed considers the PCE inflation as its favorite gauge to measure pricing pressure.

The core PCE index rose 3.1%, faster than December’s 3% rise but aligning with the consensus estimate. The January rate marked the steepest climb since March 2024.

Annual Rates of Price Consumption Expenditure Indices

Source: BEA

Separately, BEA’s second estimate of GDP showed that the U.S. economy grew at a markedly slower pace than initially estimated in the fourth quarter of 2025. The real GDP rose 0.7% quarter over quarter, down from the 1.4% advance estimate released in late February, and slower than third quarter’s 4.4% growth.

The reduction relative to the advance estimate reflected downward revisions to exports, consumer spending, government spending, and investment.

With the inflation reading supportive of dollar strength, the U.S. unit is expected to stay bid in the near term. ING strategist Chris Turner said he sees the greenback pushing to last summer’s highs of 100.25/35 region. “We cannot see investors wanting to fight this dollar rally, given there is so little certainty as to when this crisis will end,” the strategist said.

“And traders, once again on a Friday, will not want to run any short dollar balances ahead of the weekend event risk.”