U.S. producer price inflation came in hotter than expected in January, underlining the stickiness of the pricing pressure. In what is seen as a mixed reaction, the Dollar futures edged lower and T-note futures climbed despite the pick in wholesale price inflation but stock index futures moved lower.

The rate cut odds fell further following the data, with CME FedWatch tool that factors in expectations of futures traders, showing the odds of a quarter-point cut at 3.9%, down from 4.5% a day earlier.

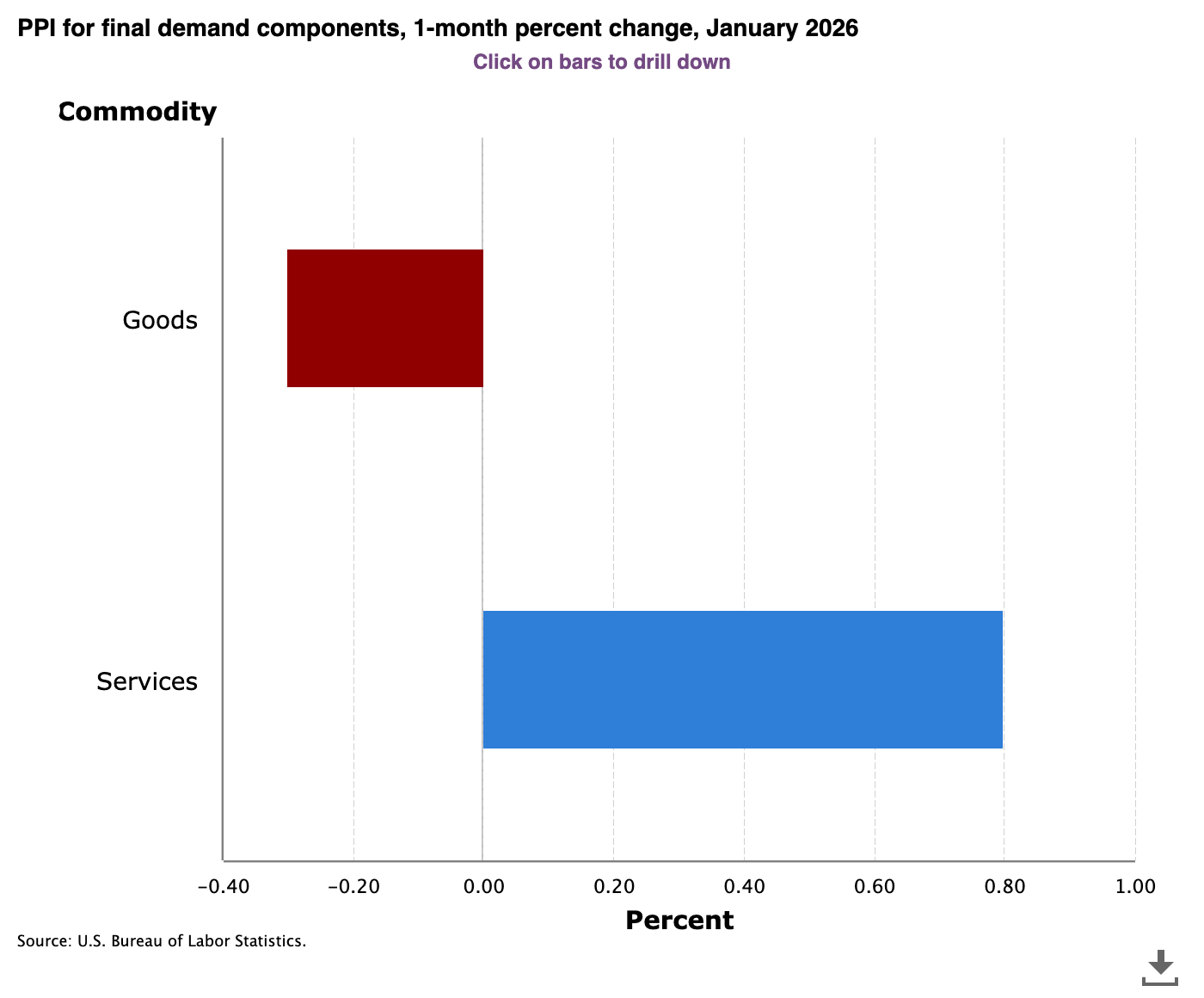

Sifting Through Numbers: Producer prices rose 0.5% month over month (MoM) versus expectations of 0.3%, according to a report released by the Bureau of Labor Statistics on Friday. This marked the quickening from the downwardly revised 0.4% pace in December. The acceleration reflected an increase in services prices (up 0.8%), while goods prices fell 0.3%.

Source: Bureau of Labor Statistics

The core producer price inflation (PPI) rate was 0.3%, flat with December's reading, which was initially reported as 0.7%.

The annual producer price inflation rate was 2.9%, slower than the 3% pace in December and exceeding the economists’ estimate of 2.6%. The January core producer prices climbed 3.4% compared to the 3.5% increase in December.

The January consumer price inflation (CPI) released earlier this month showed the monthly and annual rates ticking down from the month-ago levels and also coming in a touch softer than expected. The annual CPI rate marked the slowest since April 2025. The core readings aligned with expectations.

Policy Implications: Fund manager Louis Navellier said the January inflation reads better when goods prices are taken into account. “ A 2.5% surge in trade services distorted the PPI, just like it did in December when it rose 1.8%,” he added.fin

The next meeting of the rate-setting Federal Open Market Committee (FOMC) is scheduled for March 17-18. Between now and then, a few key first-tier economic data are due, with the February non-farm payrolls and CPI reports being the key among them.

While there is political pressure to take the Fed funds rate lower, most Fed officials have issued hawkish commentaries, preferring to keep rates higher for longer until the sticky inflation pressure budges. Atlanta Fed President Raphael Bostic, whose term ends this month, shrugged off weak labor market signals, stating that the U.S. is in a structurally high unemployment era due to the increase in labor productivity, catalyzed by artificial intelligence technology becoming all-pervasive.

President Donald Trump’s nomination of former Fed official Kevin Warsh for the Fed Chair role has also added strength to a hawkish policy outlook.

Read Next: Cooling Inflation Likely to Keep BoJ Cautious, Yen Futures Seen Range-Bound Ahead of Spring Data