Manufacturing activity stalled in the New York region in March, according to a survey released by the Federal Reserve Bank of New York. The soft reading comes as the Federal Reserve prepares to announce its latest monetary policy decision.

The survey was conducted between March 2 and March 9, and the results may have factored in manufacturers' sentiment toward the fallout from the ongoing U.S.-Iran war that started on Feb. 28 and has lasted for 17 days now. The oil supply shock due to the closure of the Gulf of Hormuz sent West Texas Intermediate (WTI) crude futures (CL) soaring to nearly $120 a barrel but there has been a slight let up since. Yet, the front-month oil futures traded at nearly $94 a barrel.

Following the survey data, the E-mini S&P 500 futures (ES) and 10-year T-Note futures (ZN) have added to their early gains, while the Dollar Index futures (DX) have added to their losses.

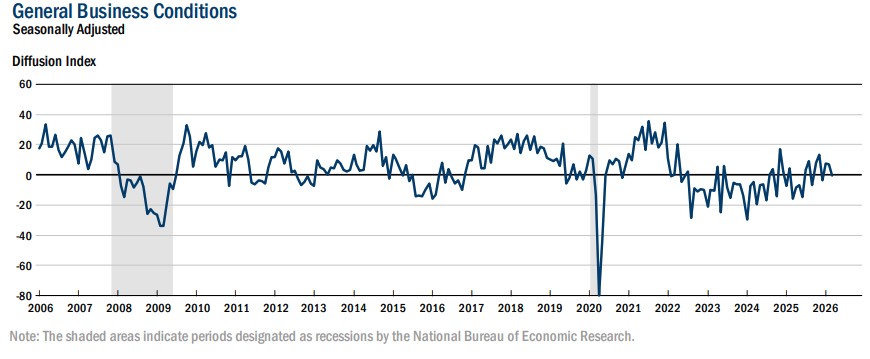

Dissecting March Numbers: The March headline business conditions index from the Empire State manufacturing survey fell to -0.2 versus 7.1 in February, while economists forecast a reading of 4 for the month.

Source: New York Federal Reserve

Among the other indices:

- New orders index: up 0.6 points to 6.4

- Shipments index: down 5.9 points to -6.9

- Unfilled orders: up 1.7 points to 10.8

- Delivery time: jumped 9.7 points to 13.7

- Inventories: down 0.2 points to 6.9

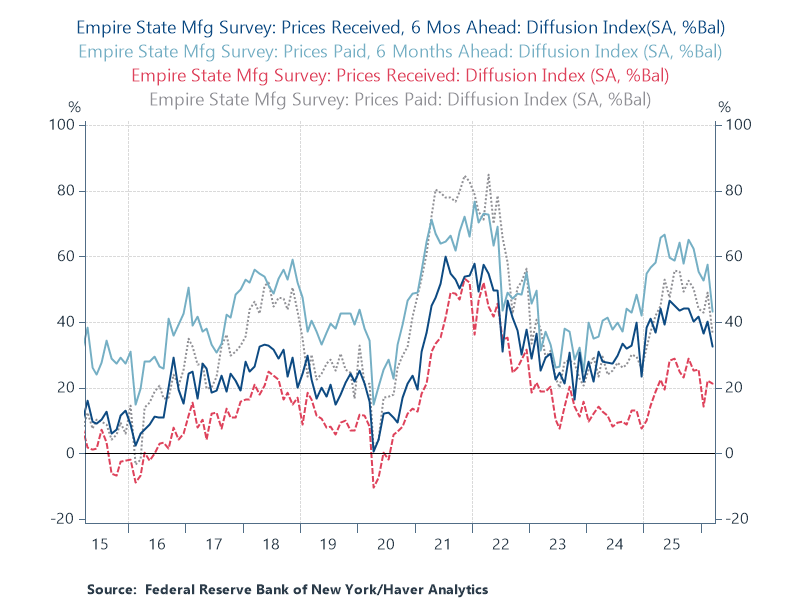

- Prices paid: slumped 12.5 points to 36.6

- Prices Received: down 0.8 points to 21.4

- Number of employees: up 1.8 points to 5.8

- Average Employee Workweek: down 0.2 points to 1.9

- Supplier Availability: down 2.9 points to -1

Manufacturers Hold Optimistic Outlook: The future business conditions index, although down 5.8, remained in positive territory at 31. A reading above “0” indicated improvement in conditions. New orders and shipments are expected to increase, and employment is expected to grow in the months ahead.

The capital expenditures (Capex) index rose three points to 21.6, a multi-year high, suggesting strength in investment.

Commenting on the data, Renaissance Macro Research stated that said price measures have seen improvement despite the war, with the prices paid slipping to the lowest level since January 2025.

Price Indices of Empire Fed Survey

NY Fed data via RenMac X account

Manufacturing Output Outperforms: A Federal Reserve report released Wednesday showed that manufacturing output edged up 0.2% month-over-month in February. This exceeded the 0.1% growth estimated by economists but marked a slowdown from January’s downwardly revised 0.6% rate (initially reported as 0.8%).

Mining output growth decelerated slightly to 0.8% from 0.9%, while utilities output fell 0.6%, reversing the 0.1% growth in January.

The year-over-year industrial output growth slowed to 1.4% in February from the previous month’s 2.3% rate.

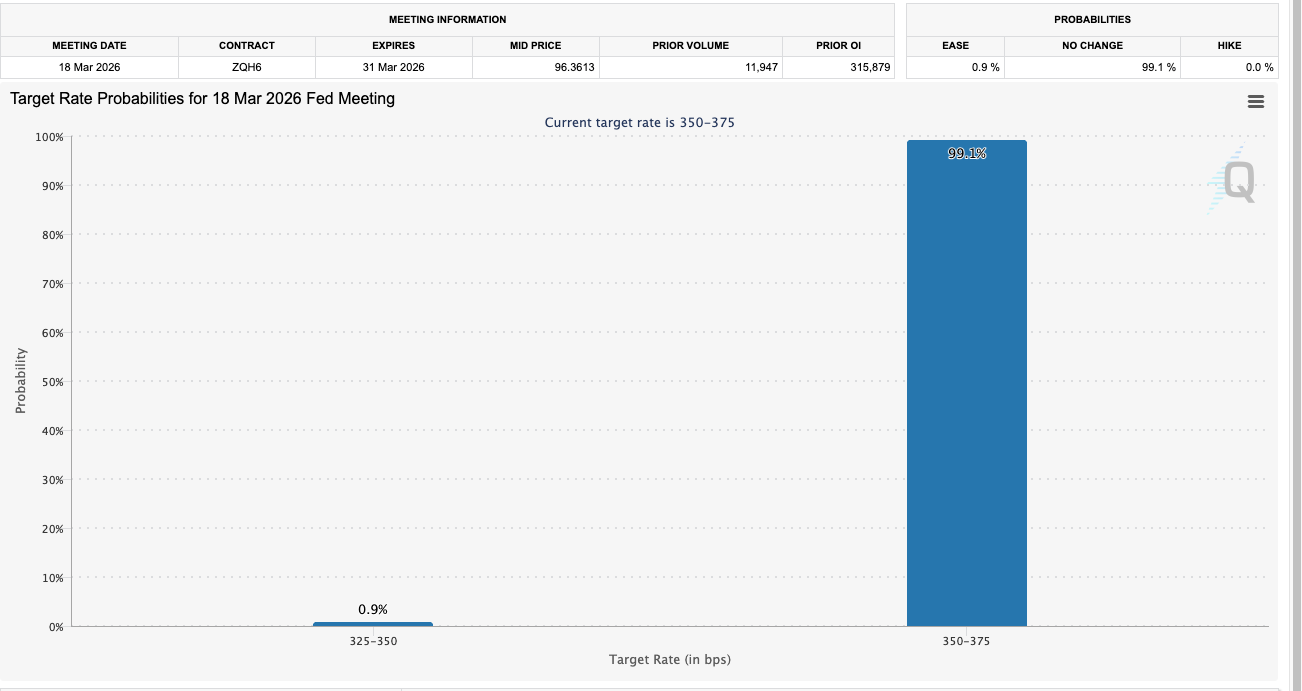

What’s Next for Futures Traders: The spotlight now shifts to the upcoming two-day Federal Open Market Committee (FOMC) meeting, which begins on Tuesday. According to the CME FedWatch Tool, the probability of a quarter-percentage-point cut to the Federal Funds Rate is currently less than 1%.

CME FedWatch Tool

Source: CME Group

The minutes of the January FOMC meeting showed that several participants felt rate hikes could even be appropriate.

Delving into the potential outcome, Raymond James’ Wealth Management business Peck Bulgin Chief Investment Officer Larry Adam said a Fed pause is all but certain. “The Fed’s usual playbook is to ‘look through’ oil shocks, but the post‑COVID lesson that inflation wasn’t as transitory as expected still looms large,” the strategist said. Fresh geopolitical risks and their inflationary potential have come at a time when FOMC members are leaning toward hawkishness.

That caution showed up in the January meeting minutes, where several Federal Open Market Committee (FOMC) members suggested rate hikes could be on the table if inflation fails to return to the 2% target. Against that backdrop, fresh geopolitical risks and their inflationary potential are arriving at a particularly inopportune time given this hawkish shift.

Read Next: More Evidence of Sticky Inflation Drops Even As Growth Disappoints — Stagflation Risk Looms?