A Federal Reserve official said on Monday that the U.S. labor market is the missing piece of the jigsaw puzzle that could determine which way the central bank’s policy-setting Federal Open Market Committee (FOMC) is headed in March.

After reducing the Fed funds rate by quarter-points for three straight meetings late last year, the central bank deemed it fit to hold fire at the January meeting.

In prepared speech delivered at the 42nd Annual National Association of Business Economics (NABE) Policy Conference held in Washington D.C. on Monday, Fed Governor Christopher Waller delved into the host of issues including the impact of the Trump tariff annulment, and the state of the labor market.

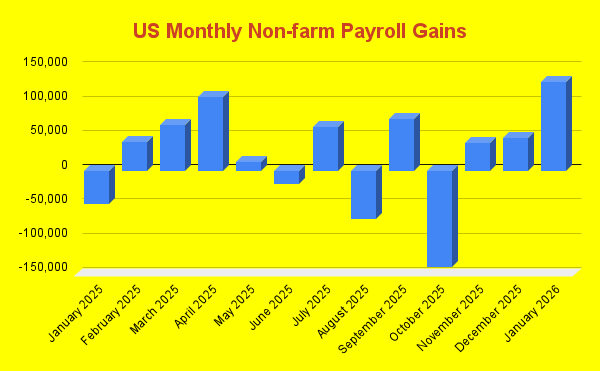

Inconclusive Labor Market Evidence: Waller, who was among the two dissenters at the January meeting, rooting for a quarter-point cut, said one month of good news does not constitute a trend. The Fed official was referring to the January non-farm payrolls data, which showed gains of 130,000 for January.

Data Source: BLS

“We will not know whether the upturn in this initial estimate of job creation is signal or noise until we get more data,” Waller said. “If these data support the idea of an improvement in the labor market in January that continued in February, along with additional progress toward 2 percent inflation, that could result in my outlook turning a bit more positive and my view of appropriate monetary policy may tilt toward a pause at our upcoming meeting.”

That said, Waller also suggested a rate cut is not off the table. “But even if inflation continues to make progress toward 2 percent, if the new labor data dent the idea of a turnaround and instead point to continued weakness like we saw in 2025, then there may be an equally credible case for a further reduction in the policy rate.”

Growth Outlook: The Fed Governor expressed confidence in the economy returning to 2%+ growth in the first quarter of 2026, following a slowdown to a 1.4% in the fourth quarter of last year. He expects the government shutdown, which reduced growth in the final three months of last year, to boost growth in the next three months.

Tariff Impact: Waller said traditional central bank wisdom calls for looking through the tariff noise. While conceding that the Supreme Court ruling, striking down the tariffs, may impact near-term price increases, he said it may have only a transitory effect on inflation. “So, this ruling is unlikely to have a significant impact on my view of the appropriate stance of policy,” he added.

Monetary Policy Outlook: Waller considers the February inflation report, due on March 11, and the February labor report as the important data for his judgment on the appropriate monetary policy stance. The Fed officials believe if inflation continues to head back toward the Fed’s 2% target, the key to setting appropriate monetary policy will be the labor market. Here’s how his decision would pan out:

- If downside risks to the labor market have diminished (strong February payrolls and low unemployment rate), it would be appropriate to maintain the status quo stance.

- If January payroll gains are revised away or evaporates, a 25-basis-point cut would be appropriate at the March meeting.

Waller, however, feels as of now the two potential outcomes are close to a coin flip.