U.S. treasuries showed muted reaction to reports of Chinese move to curb purchases of American bonds. Yields across the maturity duration were mixed in Monday’s session.

What’s brewing in China: A Bloomberg report, citing people familiar with the matter, stated that Chinese officials had required banks to limit their purchases of U.S. government bonds. They have also asked those banks with high exposure to lighten their holdings. Bloomberg stated that China attributed the mandate to the need to diversify risk.

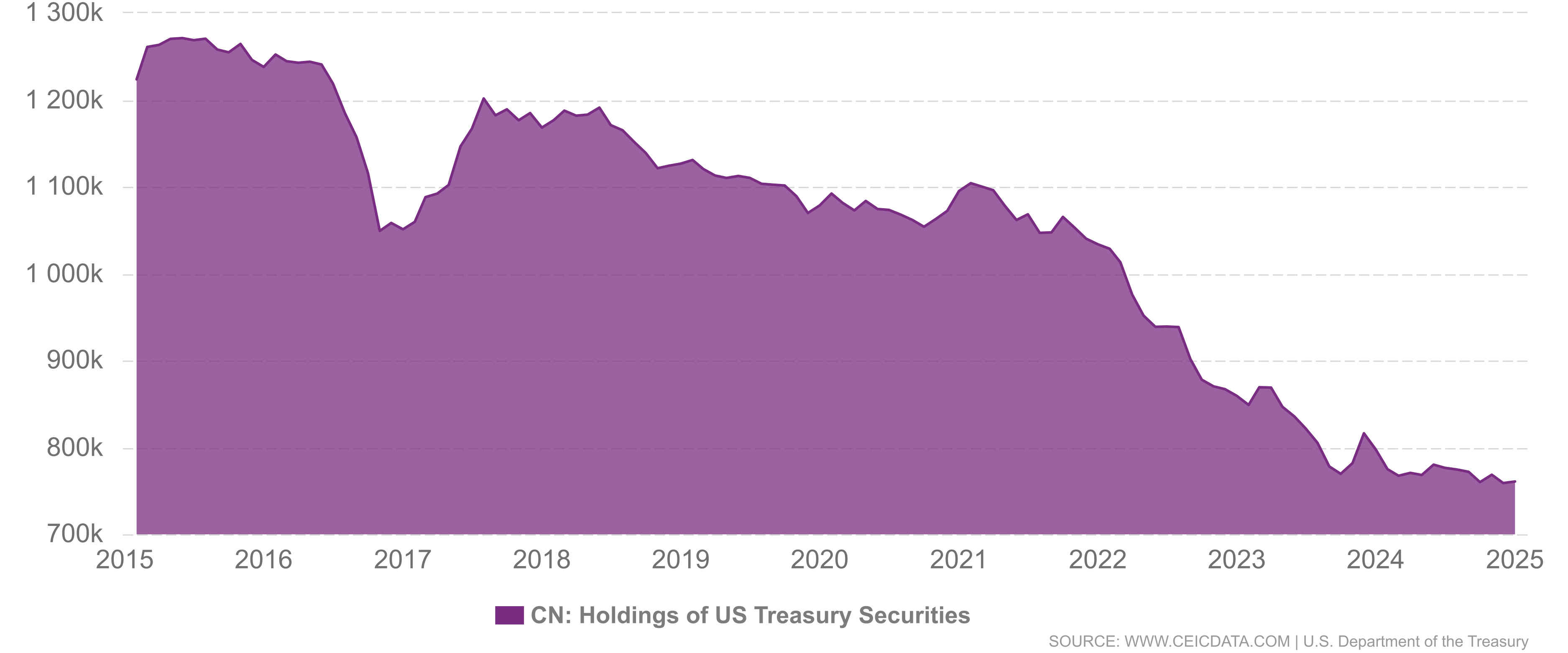

The timing and size cap, however, hasn’t been communicated yet, and the restriction does not reportedly apply to China’s state holdings of treasuries. Nonetheless, China’s holding of the U.S. Treasuries have dropped steeply over the past few years. From nearly $1.3 trillion in 2015, China’s treasury holdings have dropped to $682.6 billion in Nov. 2025. The world’s second-largest economy, however, was the third-largest holders of U.S. treasuries.

Source: US Treasury Department via CEIC Data

Here’s how the Treasury futures are trading:

- ZT (2-Year T-Note Futures): up 0.03%

- ZF (5-Year T-Note Futures): up 0.02%

- ZN (10-Year T-Note Futures): flat

- ZB (U.S. Treasury Bond Futures): down 0.19%

- UB (Ultra U.S. Treasury Bond Futures) - down 0.29%

Is US Treasuries’ Safe Haven Appeal Waning? Once considered the highest form of safe-haven asset, the appeal of U.S. treasuries have been slowly and steadily waning. Treasuries typically are considered as crisis hedges, which retain their value or appreciate during periods of geopolitical and economic stress. Investors have now come to be less confident of U.S. assets following the geopolitical, and economic uncertainties set in motion by the Trump administration. Nevertheless, it still wields the clout.

In a July 2025 report, Raymond James stated that “there is no other market that matches the size, liquidity, depth or global influence of the US Treasury market.” The firm noted that the U.S. Treasury market, at $28.5 trillion, is roughly equivalent to the combined government bond markets of China, Japan, UK, France, Italy and Germany.

Implications for futures traders: If foreign demand continues to erode, the longer-date maturities will suffer relative to their shorter-term counterparts. A futures trader can consider overweighting ZN and underweighting ZB/UB.

Another approach is to sell the rallies in ZB, which is the most-duration sensitive. Also, sell ZN only if the weakness seen in the longer dated bonds spreads to the 10-year T-note.