A preliminary report from the University of Michigan showed that consumer sentiment edged up in February, although remaining sharply below year-ago levels.

Consumer Morale Ticks Up: The headline consumer sentiment index improved 1.6 points to 57.3 in February, but was down 11.4% from the same period last year.

The current economic conditions index improved 5.2 points month over month to 58.3, while the expectations index slid 0.7 points to 56.6. Both readings, however, remained more than 11 points lower than their respective year-ago levels.

Consumer Sentiment survey Director Joanne Hsu said, “While sentiment is currently the highest since August 2025, recent monthly increases have been small—well under the margin of error—and the overall level of sentiment remains very low from a historical perspective.”

The stagnation of consumer sentiment at depressed levels was attributed to concerns about the erosion of personal finances from high prices and the elevated risk of job loss.

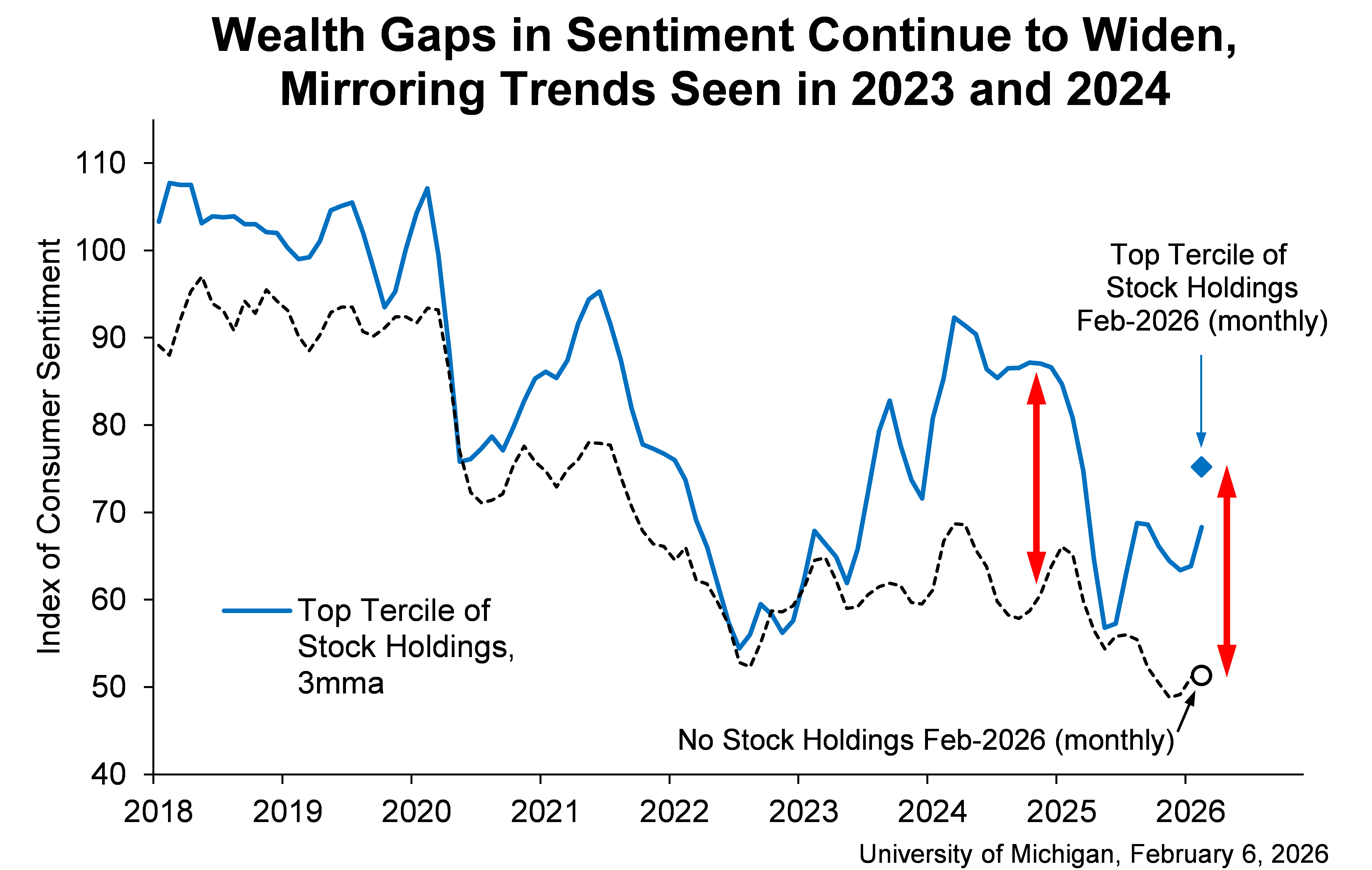

Hsu said sentiment improved notably for consumers with the largest stock portfolios. On the other hand, the sentiment of consumers without stock holdings remained at dismal levels. On net, modest increases in current personal finances and buying conditions for durables were offset by a small decline in long-run business conditions.

Source: University of Michigan

Inflation Expectations Wane: Inflation expectations for a year ahead slipped back to 3.5% from 4% in January, marking a one-year low. Nevertheless, February’s reading still exceeded the levels seen in 2024 and remained well above the 2.3%-3.0% range seen in the two years pre-pandemic.

Long-run inflation expectations (5-year) inched up for the second straight month, to 3.4% from 3.3%. The metric ranged between 2.8% and 3.2% in 2024, and were below 2.8% throughout 2019 and 2020.

The final reading for February is due at 10 a.m. ET.

Economist’s Take: “Clearly, the wealth effect remains a key factor for consumer spending and consumer expectations,” said LPL Chief Economist Jeffrey Roach. “Consumers have moved on from tariff preoccupations. Higher assets improved the outlook for household finances, i.e., the K-shaped economy continues.”

The economist noted that more consumers say “it’s a good time to buy a vehicle and major household items.” He, therefore, expects real growth to approach 2.7% in the first quarter.