Two separate readings on Thursday added to evidence pointing to recovery in the labor market conditions, although the green shoots of recovery are yet to take a firm hold. The data did little to lift sentiment toward equities, with the stock index futures continuing to wallow in negative terrain.

The dollar Index futures (DX), however, gained ground, potentially due to the ongoing geopolitical tensions in the Middle East, perking up the appeal of the safe haven greenback. Bond prices fell across the maturity spectrum.

So what did the labor market data tell us?

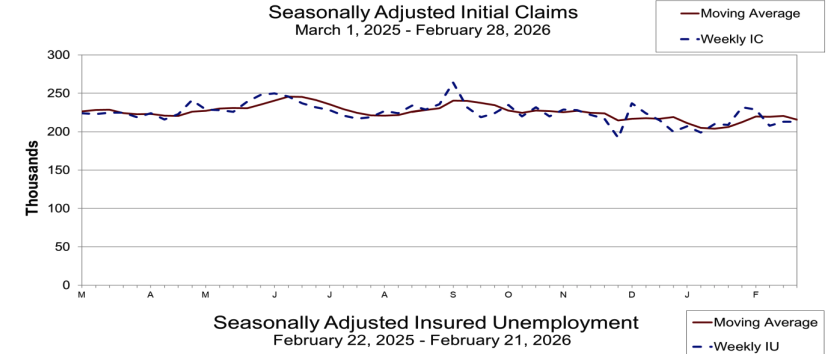

Claims flat: The number of individuals claiming unemployment benefits was 213,000 in the week ended Feb. 28, according to a Bureau of Labor Statistics’ (BLS) report. Economists, on average, had expected claims to increase to 215,000 from the initially reported 212,000 for the previous week’s reading, which revised up by 1% from the initially reported 212,000 for the previous week.

The four-week average, which smooths volatility, declined by 4,750 to 215,750 from the previous week’s revised average.

Source: Department of Labor

Continuing claims, which is calculated with a week’s lag, however, climbed 46,000 to 1.868 million. This measures the total number of residents receiving ongoing unemployment benefits, having filed their initial claims at least in one week previously. Commenting on the number, veteran trader Naeem Aslam said the rise in the continuing claims to a nearly five-month high shows that some workers are taking longer to find new jobs.

That said, the initial claims of sub-220,000 aligned with the unemployment rate under 4.2%, he said, adding that this reduces the pressure for the Federal Reserve to reduce rates.

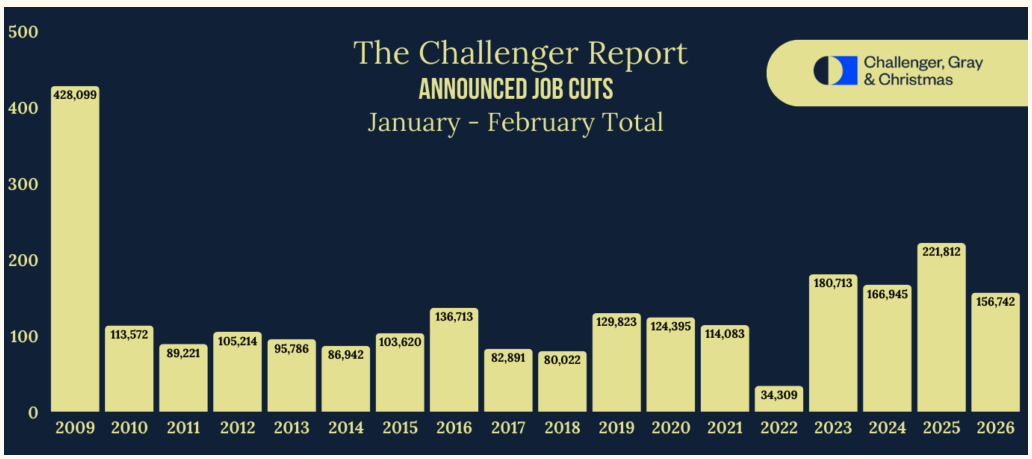

Hirings Lackluster, Firings Fall: A separate report released by outplacement and executive coaching firm Challenger, Gray & Christmas showed job cuts in the U.S. plunged 55% month over month in February to 48,307. About a quarter of the cuts were in the technology sector.

The January-February total firings are the lowest for the first two months of the year since 2022.

Source: Challenger, Gray & Christmas

Andy Challenger, workplace expert and chief revenue officer for Challenger, Gray & Christmas, said, “February’s dip is a nice reprieve from the elevated job cut plans to start the year. With U.S. involvement in a growing war in Iran, the end of Q1 may bring more layoff plans as companies tighten belts amid uncertainty and higher costs.”

On the other hand, hiring plans rose 140% in February to 12,755 from 5,306 in January, but are down 63% from year-ago period.

Separately, a preliminary report released by the Labor Department showed non-farm productivity rose 2.8% quarter over quarter (QoQ) in the fourth quarter, slower than the 5.2% jump in the previous three-month period. The productivity growth, however, exceeded economists’ estimate of 1.9%.

Unit labor costs climbed 2.8%, reversing some of the 1.8% drop in the third quarter, faster than the 2% rate expected by economists.

NFP Report In Spotlight: The CME FedWatch tool now puts the odds of a hold decision later this month at 97.3%. Traders now turn their attention to Friday’s non-farm payrolls report to get additional clarity on the state of the labor market. Economists, on average, estimate job gains of 58,000 for February, slower than the 172,000 additions in January. The jobless rate is expected to hold steady at 4.3%.

Read Next: China Sets Slowest Growth Goal Since 1991, Adding a Macro Headwind for Global Futures Traders