Risk-off mood prevailed in equity markets as the Middle East tensions continued to escalate with the opening of a third front in the U.S.-Iran war. Yemeni Houthis jumped into the fray in solidarity with their ally Iran and launched attacks on Israel and strategists see the development as an escalation of the current crisis that could lead to a regional war, disrupt shipping through the Red Sea Corridor, which has key chokepoints Suez Canal, and Bab el-Mandeb Strait.

Traders chose to sell risky bets as crude oil prices pushed higher with renewed vigor and fears of the month-long war prolonging mounted.

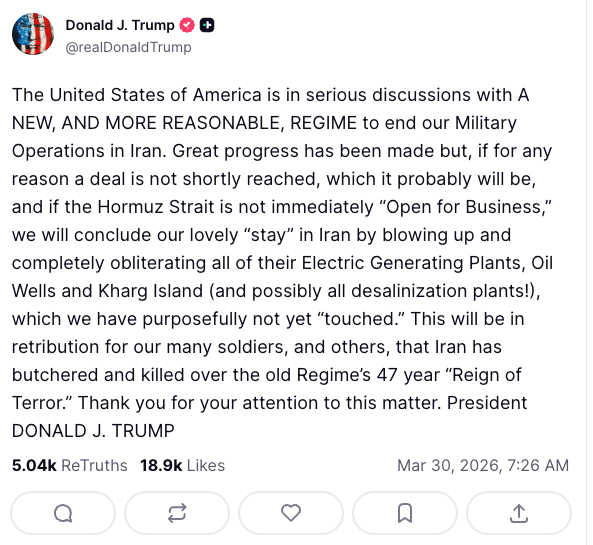

Deal or No Deal? In an early Tuesday post, U.S. President Donald Trump sent conflicting messages regarding the war trajectory. As the war entered its 31st day, Trump said the U.S. was in serious discussions with a “new, and more reasonable, regime” to end the war and that “great progress has been made,” a claim he had made earlier too.

He also threatened “blowing up and completely obliterating all of their Electric Generating Plants, Oil Wells and Kharg Island (and possibly all desalinization plants!)” if the Strait of Hormuz was not opened for business.

NQ Futures Deepen Losses: As uncertainty around any resolution abounds, the E-mini contract tied to the Nasdaq 100 Index (NQ) appears on track to finish lower for the third straight session. On Friday, the NQ futures and the underlying Nasdaq 100 Index entered into correction territory, defined as a 10% drop for any financial asset from its recent high.

The contract is holding near a basing pattern from last August. Failing to hold support around this level could lead to a deeper sell-off, all the way to the 22,000 level.

NQ Futures (1-Year Chart)

Chart courtesy of TradingView

Time to Buy Dip? Morgan Stanley Equity Strategist Michael Wilson sees light at the end of the tunnel. There’s “Growing evidence the S&P 500 correction is getting closer to its ending stages,” he said. He premised his deduction on the 17% compression in S&P’s forward price-earnings (P/E) multiple, which is in the range of the prior growth scare outcomes in the absence of a recession or hiking by the Federal Reserve.

Wilson said unlike during the earlier oil shocks, earnings per share (EPS) growth is accelerating. He also noted that the year-over-year (YoY) move in oil is about half of what it was during the previous oil shocks.

Morgan Stanley recommended having exposure to quality names as it expects volatility to persist in the near term, particularly due to the risk of rate hike.